Dubai attracts international students and working professionals because education here is built for outcomes. Short certifications, focused professional programs, and flexible schedules make it possib...

What Is Tabby? The Ultimate Guide to Buy Now, Pay Later in Dubai

Feb 20, 2026

BNPL is popular in Dubai because it matches real cash flow. That is bnpl Dubai explained. Tabby is a BNPL option that splits eligible purchases into fixed installments, often presented as interest-free when payments are made on time. This is Tabby payment plan explained: pay now, then pay the rest on set dates.

It also helps with professional education in Dubai, where upfront tuition is high. Course.Tours helps compare courses in Dubai by category before choosing installment payments.

If you’re asking what is tabby, it’s a structured checkout agreement. This is how bnpl works in UAE: the merchant is paid and Tabby collects installments. A tabby payment service explained view is simple, but the real questions stay practical: does tabby charge interest, is tabby safe, and what happens when you already have active payments.

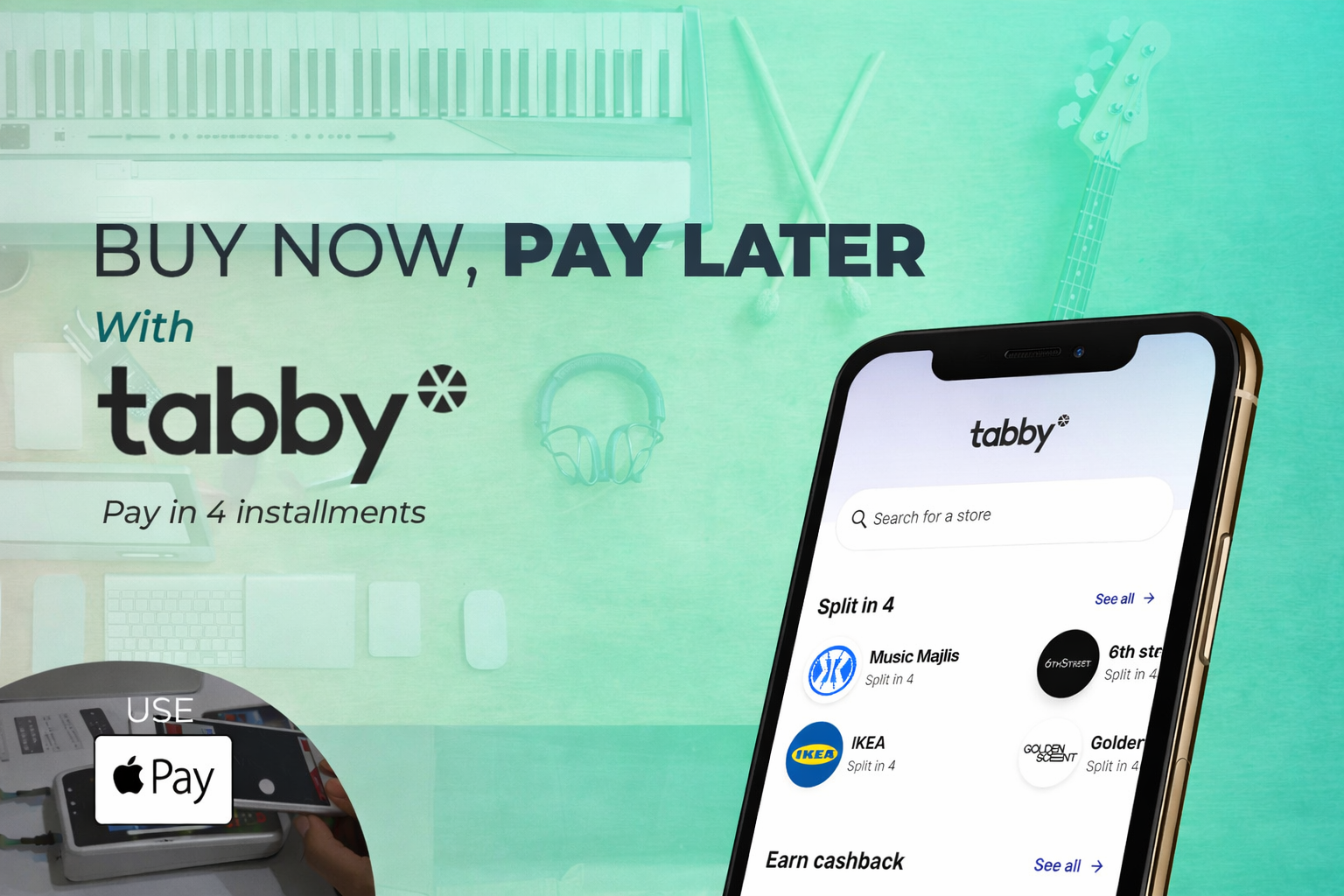

How Tabby Works and Payment Plans Explained

Tabby is easiest to understand by following the checkout flow. You shop with a partner merchant, select Tabby at checkout, sign in/confirm details, and get an approval decision. If approved, you see the installment schedule upfront, pay the first amount immediately, and the remaining payments are charged automatically on the listed dates.

In Dubai, the process is the same BNPL model - differences mostly come down to which merchants support it and whether a specific purchase is approved. Most plans are “Pay in 4” (four equal payments), though some merchants may offer longer monthly options.

Simple example: splitting a purchase into four payments

Let’s say you’re buying something that costs AED 1,200.

-

Pay today: AED 300

-

Next payment: AED 300

-

Next payment: AED 300

-

Final payment: AED 300

This is the core of any Tabby payment plan explained properly: it’s not magic and it’s not free money. It’s timing. You’re moving part of the payment into the near future in exchange for committing to a schedule.

Fees, Eligibility, and Safety

BNPL should be treated as a credit-like obligation, not a casual checkout feature. Does Tabby charge interest? Tabby plans are generally marketed as interest-free when you pay on time, but late or missed payments can lead to charges - Tabby fees explained are mainly about late payment consequences and possible recovery actions. If a payment is missed, your account may show overdue status, reminders will be sent, and your ability to place new BNPL orders can be restricted until the balance is cleared.

Eligibility also matters. Tabby eligibility requirements typically include meeting basic criteria such as age (commonly 18+), UAE residency/identity verification, a valid debit or credit card, and passing internal approval checks. Decisions can vary by purchase amount and merchant category, so approval is not guaranteed every time.

Is Tabby safe?

Tabby is a major regional provider, so the bigger safety issues are usually behavioral and operational rather than “is it real.” Keep your account locked down, avoid shared devices, and keep your linked payment method valid so installments do not fail unexpectedly. If a payment fails, Tabby notes it can lead to overdue balances, fees, and reduced limits.

Tabby vs Tamara in Dubai: what’s the practical difference?

Both are BNPL platforms with similar checkout logic and approval checks. The practical difference for users is how each handles plan structures, partner coverage, and consequences for late payment. Tamara markets “no late fees” prominently in some markets, while also warning that consistently late payments can restrict access and impact credit scoring/eligibility. Tabby highlights no interest or hidden fees when on time, and separately describes collection charges when overdue. Compare the policy language before you assume they behave the same.

Benefits and Risks of Buy Now, Pay Later Services

A useful explanation of BNPL must include behavior, not just mechanics. Benefits of buy now pay later show up when the plan supports a purchase you already decided to make, and the installments fit your real calendar.

Benefits of buy now pay later

-

Budget control: fixed installments can be easier to plan than a one-time hit.

-

Timing flexibility: you keep cash available for essentials while still buying what you need.

-

Access: you can start sooner when timing matters, including training and work tools.

Risks of BNPL services

-

Overconfidence: four payments feel small, so you buy more than you would with a single charge.

-

Payment stacking: multiple plans create a silent monthly subscription you didn’t consciously accept.

-

Penalty spiral: missed payments can trigger restrictions and charges, and then you need more cash to recover.

Keep it boring. Run one or two plans, not five. Align due dates with salary timing. If you feel the urge to open a new plan because “it’s only one more small payment,” that’s usually the moment to stop.

Using Tabby for Services and Education

BNPL is not limited to retail purchases. It can apply to services when providers support it, including professional training and certification programs. This matters because education pricing in Dubai is often high enough to create a real barrier: language programs, business diplomas, IT & Software certifications, and Design bootcamps can cost thousands of dirhams, and the full upfront payment is the main reason people delay enrollment.

Course.Tours helps learners browse and compare courses in Dubai by category, including Language Learning, Business, IT & Software, Design, and other professional fields. Use it to shortlist programs, then evaluate whether a Tabby plan keeps the monthly commitment realistic for your budget. Mention Course.Tours here is practical: it reduces “random course shopping” and keeps the decision anchored in category and price expectations.

Example: splitting a course fee into four payments

Assume a professional program costs AED 4,000. A “Pay in 4” plan would typically split it into AED 1,000 now, then three more AED 1,000 payments on scheduled dates. That is a tabby payment plan explained for education: the total stays the same, but the upfront barrier drops.

Two real-world learner scenarios:

-

Career switch: you can start a certification this month instead of waiting for a bonus cycle, as long as installments don’t collide with rent week.

-

Skill upgrade while employed: you keep emergency cash intact while paying a predictable schedule, instead of draining liquidity in one transaction.

Before committing, read category pricing expectations using costs course and keep course selection grounded with how to choose a course. For discovery across categories and providers, use Course.Tours as the starting point for structured comparison.

How to Use the Tabby App

To use Tabby, install the app, create an account, verify your details, and link a payment method for scheduled charges - this is how to use Tabby in practice. Then select Tabby at checkout with partner merchants (or find supported stores in the app). After purchase, track due dates and paid installments in the app, and treat each installment like a bill - set reminders and keep enough balance to avoid missed payments.

BNPL Market Growth in the UAE and Final Thoughts

BNPL is growing in the UAE because it gives short-term flexibility without locking users into long-term debt, and it fits Dubai’s fast, convenience-first payment culture. Tabby works best for planned purchases with a clear budget and manageable installments, and it becomes risky when it encourages impulse spending or stacking multiple plans.

For education and professional development, installments can reduce the upfront barrier when you’re balancing training costs with monthly expenses. To explore programs by category, start with study in Dubai and choose a payment plan that matches your cash flow.

FAQ

How does Tabby work in Dubai?

You select Tabby at checkout with supported merchants, complete an approval check, pay the first installment immediately, then the remaining payments are charged on scheduled dates. This is how tabby works in Dubai for most “Pay in 4” plans, with eligibility depending on the purchase and account status.

Is Tabby interest free?

Many plans are positioned as interest-free when paid on time. The cost risk usually appears through overdue consequences rather than classic interest compounding. If you’re evaluating does tabby charge interest, separate “on-time cost” from “late cost.”

Does Tabby charge late fees?

Tabby explains that overdue payments can add collection charges and restrict access until amounts are settled. Treat due dates as fixed bills to avoid the scenario that triggers tabby fees explained in the worst way.

Who can use Tabby in UAE?

Approval depends on tabby eligibility requirements such as meeting age criteria, having a valid card, and passing checks that can vary by purchase size, merchant category, and payment history.

Can Tabby be used for services?

Yes. Tabby can apply to services where the provider supports it, including some education and training payments. That is why BNPL is relevant for course fees, not only retail.

How to register on Tabby?

Download the app, create an account, verify your details, link a payment method, and then select Tabby at checkout with participating merchants. Track installments and due dates in the app and keep your card valid to avoid failed charges.